Generative AI Revenue and Cloud Spending Insights

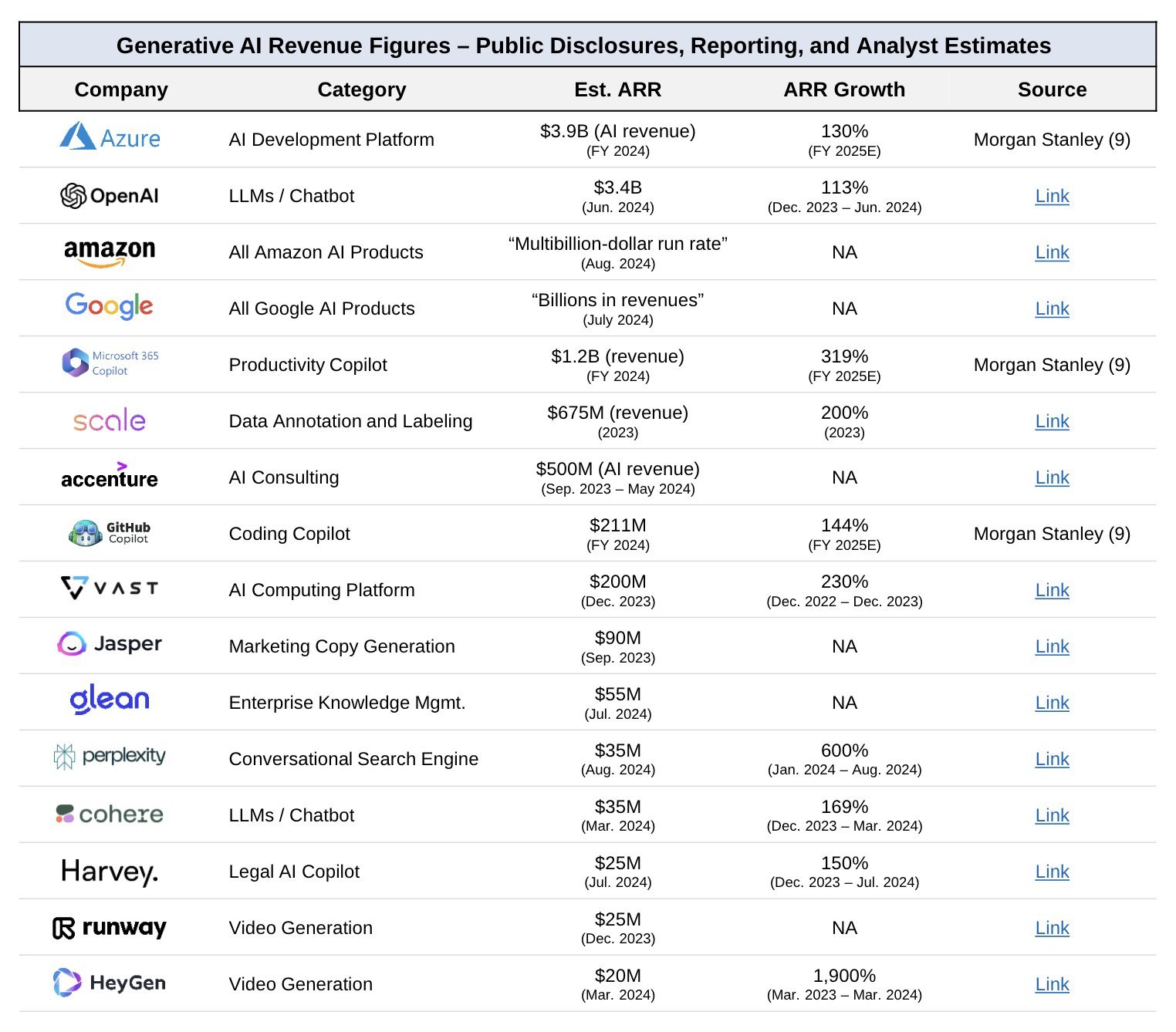

Generative AI Revenue Figures

This table provides an overview of estimated annual recurring revenue (ARR) for various companies involved in generative AI technologies, their categories, growth rates, and sources of information.

| Company | Category | Est. ARR | ARR Growth | Source |

|---|---|---|---|---|

| Azure | AI Development Platform | $3.9B | 130% | Morgan Stanley (9) |

| OpenAI | LLMs / Chatbot | $3.4B | 113% | Link |

| Amazon | All Amazon AI Products | "Multibillion-dollar run rate" | NA | Link |

| All Google AI Products | "Billions in revenues" | NA | Link | |

| Microsoft 365 | Productivity Copilot | $1.2B | 319% | Morgan Stanley (9) |

| Scale | Data Annotation and Labeling | $675M | 200% | Link |

| Accenture | AI Consulting | $500M | NA | Link |

| GitHub Copilot | Coding Copilot | $211M | 144% | Morgan Stanley (9) |

| VAST | AI Computing Platform | $200M | 230% | Link |

| Jasper | Marketing Copy Generation | $90M | NA | Link |

| Glean | Enterprise Knowledge Mgmt. | $55M | NA | Link |

| Perplexity | Conversational Search Engine | $35M | 600% | Link |

| Cohere | LLMs / Chatbot | $35M | 169% | Link |

| Harvey | Legal AI Copilot | $25M | NA | Link |

| Runway | Video Generation | $25M | NA | Link |

| HeyGen | Video Generation | $20M | 1,900% | Link |

Summary of Points:

-

Azure's Dominance: As a significant player in the AI development platform space, Azure's estimated ARR of $3.9 billion showcases its potential in the cloud computing and AI integration markets, projected to grow 130% by 2025.

-

OpenAI's Growth: OpenAI continues to show robust growth with an estimated $3.4 billion ARR for LLMs and chatbots, reflecting the increasing demand for conversational AI solutions.

-

Amazon and Google: While Amazon and Google report broad multi-billion dollar revenue runs, they haven't provided specific figures, indicating their extensive portfolio of AI products might be harder to quantify individually.

-

Microsoft's Strong Position: With an estimated $1.2 billion ARR from its productivity copilot, Microsoft highlights the efficiency gains AI can provide in business settings, coupled with a remarkable growth projection of 319%.

-

Scale's Expansion: The data annotation and labeling market is critical for training AI models, and Scale's growth to $675 million ARR (200% growth) indicates a booming need for data preparation services.

-

High Growth Companies: Companies like Perplexity and HeyGen exhibit extremely high growth rates (600% and 1,900% respectively), suggesting niche markets within AI are rapidly evolving and attracting significant investments.

-

Consulting Services: Accenture, with its AI consulting service estimated at $500 million, underscores the importance of supporting businesses in integrating AI technologies into their operations.

This data reveals the dynamic landscape of generative AI, showcasing established companies and emerging players while indicating substantial growth potential across the sector.

Reference:

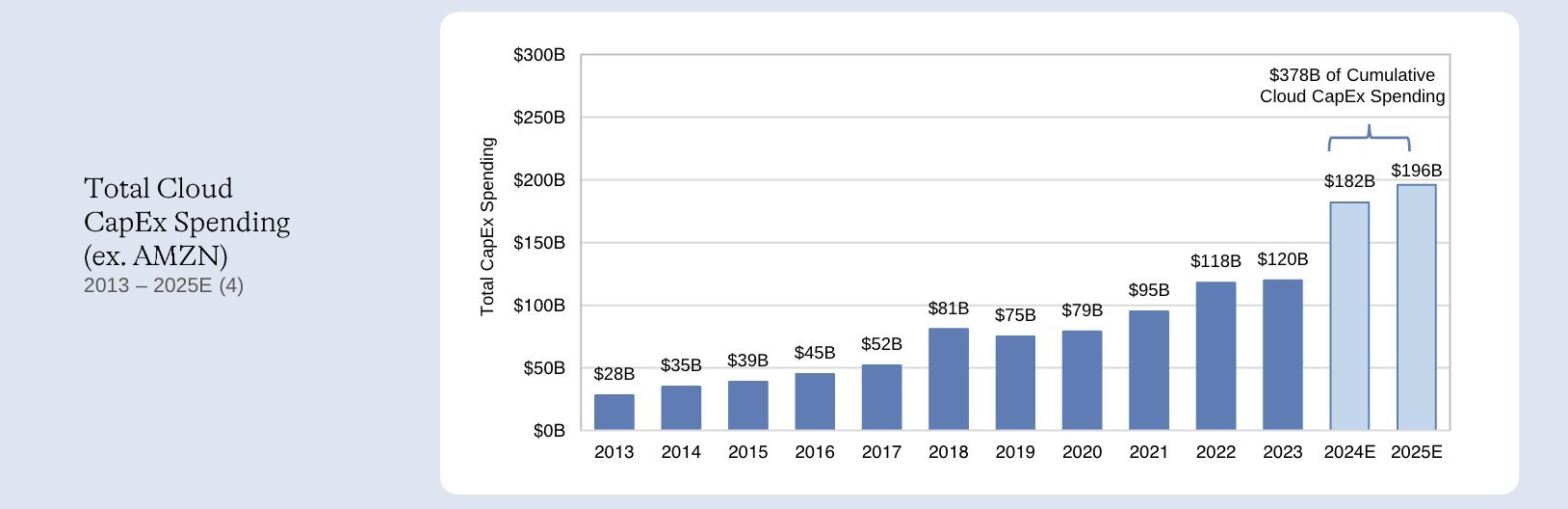

Total Cloud CapEx Spending (ex. AMZN) 2013 – 2025E

Overview

- The graph illustrates the total capital expenditures (CapEx) on cloud services (excluding Amazon's spending) from 2013 to estimated figures for 2025.

- There is a noticeable increasing trend in spending over the years, indicating a growing investment in cloud infrastructure.

Key Observations

- Annual Spending Growth:

- Spending started at 95B in 2021.

- The projected spending for 2024 and 2025 is 196B, respectively, showcasing a significant upward trajectory.

Data Summary

| Year | CapEx Spending |

|---|---|

| 2013 | $28B |

| 2014 | $35B |

| 2015 | $39B |

| 2016 | $45B |

| 2017 | $52B |

| 2018 | $81B |

| 2019 | $75B |

| 2020 | $79B |

| 2021 | $95B |

| 2022 | $118B |

| 2023 | $120B |

| 2024E | $182B |

| 2025E | $196B |

Cumulative Spending Insight

- The cumulative CapEx spending is projected to reach $378B by the end of 2025. This figure reflects the total investments made over the entire period from 2013 to 2025, emphasizing the importance of cloud infrastructure in the tech landscape.

Implications

- The consistent increase in CapEx spending suggests robust demand and a shift towards cloud-based solutions across industries, potentially driven by digital transformation trends and the expansion of services offered by cloud providers.

- Understanding these trends can help businesses strategize their cloud investments and gauge market opportunities in the expanding cloud technology sector.

Reference:

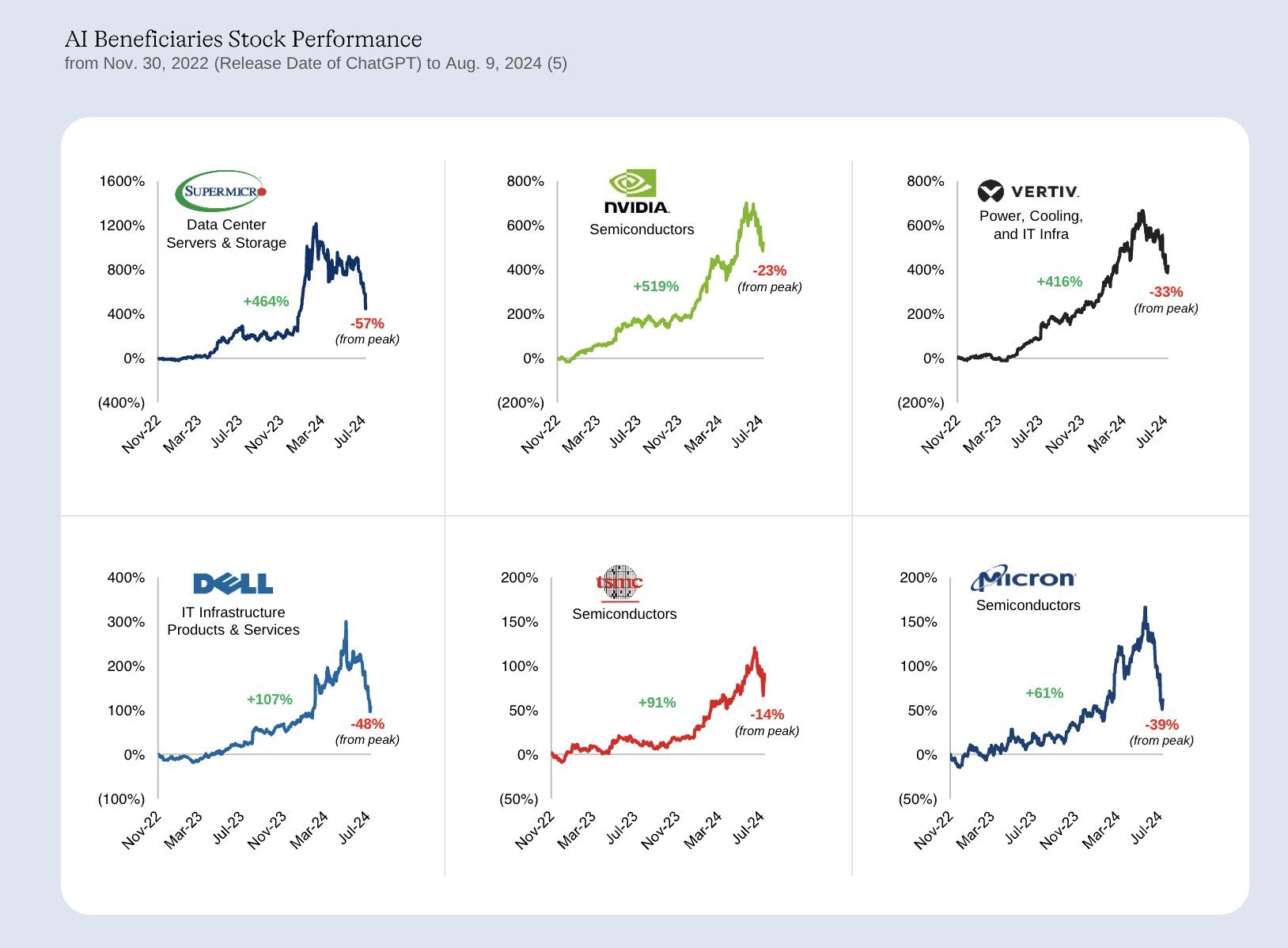

AI Beneficiaries Stock Performance

Overview

The image presents a comparison of stock performance for various companies significantly impacted by AI developments from November 30, 2022, to August 9, 2024. It highlights substantial growth in tech companies, particularly in sectors like data centers and semiconductors.

Key Points

-

Supermicro (Data Center Servers & Storage)

- Performance: +464% from Nov. 2022; sees a decline of -57% from its peak.

- Thoughts: Supermicro's growth indicates strong demand for data center infrastructure, likely driven by the AI boom. The sharp decline from the peak suggests market corrections or profit-taking.

-

NVIDIA (Semiconductors)

- Performance: +519% since Nov. 2022; declined -23% from its peak.

- Thoughts: NVIDIA, a leader in GPU technology used in AI applications, reflects the ongoing demand for AI computing power. The decline from peak performance may indicate market maturity or fluctuations in tech stock valuations.

-

Vertiv (Power, Cooling, and IT Infrastructure)

- Performance: +416% since Nov. 2022; decreased -33% from peak.

- Thoughts: Vertiv's growth is likely tied to the essential nature of cooling and power solutions for expanding data centers. The pullback from peak shows volatility in IT infrastructure-related stocks.

-

Dell (IT Infrastructure Products & Services)

- Performance: +107% since Nov. 2022; down -48% from peak.

- Thoughts: Dell's slower growth compared to others might reflect its broader portfolio and competition in AI-focused infrastructure. The significant decline from its peak indicates a challenging market or shifts in customer demand.

-

TSMC (Semiconductors)

- Performance: +91% since Nov. 2022; down -14% from peak.

- Thoughts: As a key player in semiconductor manufacturing, TSMC's growth shows robust demand for chips. The dip from peak performance may relate to broader industry challenges or supply chain issues.

-

Micron (Semiconductors)

- Performance: +61% since Nov. 2022; down -39% from peak.

- Thoughts: Micron’s slower growth indicates competitive pressures in memory markets, especially amid AI's increasing demand for high-performance memory solutions. The decline from peak highlights volatility in semiconductor stocks.

Summary Table

| Company | Sector | Performance (Nov. 2022) | Change from Peak |

|---|---|---|---|

| Supermicro | Data Center Servers & Storage | +464% | -57% |

| NVIDIA | Semiconductors | +519% | -23% |

| Vertiv | Power, Cooling, and IT Infra | +416% | -33% |

| Dell | IT Infrastructure Products | +107% | -48% |

| TSMC | Semiconductors | +91% | -14% |

| Micron | Semiconductors | +61% | -39% |